There comes a time in every investor’s journey when the growth darlings feel… exhausted. Maybe it's the 10th time you've watched Nvidia rip, or maybe you’ve finally grown allergic to “unprofitable tech companies burning cash faster than your morning toast.” Whatever it is, you're craving something different. Something with staying power. Something that doesn’t drop 30% because the CEO’s cousin tweeted a cat meme.

Enter: dividend stocks.

But wait—before you assume I’m here to wax poetic about boring utilities and blue chips that move at the pace of a sloth in molasses, hold up. This isn’t your grandpa’s dividend portfolio. We’re talking high-yield, rotation-ready, potentially market-beating stocks that aren’t just paying you—they’re playing to win.

Let’s talk about Rotation Time: the part of the cycle where smart money leaves overpriced tech and speculative fluff for value plays and income-producing assets. When interest rates are high, money actually costs something again, and suddenly, free cash flow and yield aren’t just buzzwords—they’re lifelines.

So, I’ve got 3 high-yield dividend beasts for you. These aren’t just juicy yielders—they’re stocks I believe could outperform the S&P 500 over the next few years.

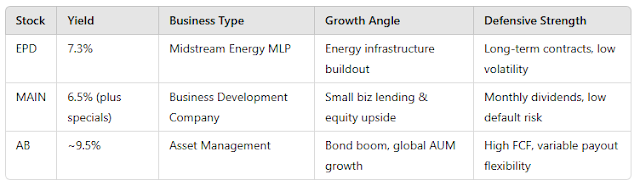

1. Enterprise Products Partners (EPD) – Yield: ~7.3%

The Income Juggernaut You’re Probably Ignoring

If I had a nickel for every time someone dismissed a pipeline stock as "boring," I could afford to buy more of this gem.

Enterprise Products Partners (EPD) is a master limited partnership (MLP) and one of the largest midstream energy companies in North America. It transports and stores natural gas, NGLs (natural gas liquids), crude oil, and refined products.

Translation: it runs the toll roads of American energy.

Why I Love It

-

Insanely consistent cash flow: With long-term contracts and volume-based revenues, EPD generates boatloads of reliable cash flow, regardless of whether oil is at $40 or $140.

-

Self-funding model: EPD doesn’t dilute unitholders with secondary offerings every quarter like it’s giving out Halloween candy. It funds its growth internally, a rarity among MLPs.

-

Distribution growth + coverage: They’ve raised their distribution for 25 consecutive years, and their current coverage ratio is over 1.6x—meaning they could cover the dividend even if the world stopped using oil for a month. (Spoiler: It won’t.)

Risks?

Sure, fossil fuels aren’t trendy. ESG funds avoid this like a leper in a hazmat suit. But let’s be real: the transition to clean energy is happening, but it’s not happening overnight. EPD is a cash cow today and will likely be one for decades.

Bottom Line

You get a rock-solid 7.3% yield, inflation-resistant revenue, and the warm, fuzzy feeling of being paid handsomely to wait.

2. Main Street Capital (MAIN) – Yield: ~6.5% (plus specials)

Wall Street in a Box—with Dividends

Main Street Capital is a business development company (BDC)—basically, it lends money to small and medium-sized businesses that banks snub like they’re holding a bag of hot garbage. In return, MAIN earns juicy interest and sometimes takes equity stakes.

Think of it as Shark Tank meets Wall Street, but with monthly dividend checks.

Why MAIN is Different

-

Internally managed: Unlike many other BDCs, Main Street isn’t lighting shareholder cash on fire with bloated management fees. The team is incentivized to create value, not churn.

-

Pristine credit performance: Their portfolio has proven incredibly resilient—even through COVID. While other BDCs had borrowers dropping like flies, MAIN kept collecting.

-

Monthly dividends: Not quarterly. Not whenever the board feels like it. Monthly. Like clockwork. And yes, they also pay special dividends a couple times a year when profits exceed targets.

Growth Potential

MAIN isn’t just a yield trap. It’s actually grown its net asset value (NAV) and dividend over time. The stock has handily outperformed the broader BDC sector—and even the S&P 500 in some periods—when you reinvest the dividends.

Risks?

It’s exposed to credit risk, especially if we enter a nasty recession. But their underwriting discipline has been A+, and their balance sheet is fortress-level solid.

Bottom Line

A 6.5% yield paid monthly, a chance at capital appreciation, and one of the best run BDCs in the game? Yeah, sign me up.

3. AllianceBernstein (AB) – Yield: ~9.5%

Wall Street’s Quiet Money Machine

You want yield? I got yield.

AllianceBernstein is a global investment manager with over $700 billion in assets under management. It serves institutions, high-net-worth individuals, and even little retail folks like you and me. And it’s paying out nearly 10%.

Wait, Why So High? Is It a Trap?

Nope. This is a case of:

-

High distributable earnings

-

Strong free cash flow

-

A variable distribution model that reflects earnings

AllianceBernstein pays a variable quarterly dividend based on its earnings and cash flow. Some people find that scary—like, "Hey, what if the dividend goes down?!"

But I find it honest.

AB doesn’t pretend it can promise a fixed 5% in perpetuity. Instead, when the business booms (like when markets surge or clients flock to fixed income in high-rate environments), it pays shareholders accordingly.

Why It Could Beat the Market

-

Booming fixed income biz: Rising rates aren’t a curse for AB—they're a windfall. They’re pulling in more clients looking for professionally managed bond portfolios.

-

Alternatives and global growth: AB isn’t just an old-school bond shop. They’ve been expanding into private markets, ESG products, and global institutional money.

-

Strong parent company: AB is majority-owned by Equitable Holdings (EQH), providing capital support and stability.

Risks?

Market cycles do matter. When equity markets tank or asset flows dry up, AB’s earnings can dip, and so does the dividend. But that’s the deal—and you’re compensated with a fat payout when times are good.

Bottom Line

If you're comfortable with some variability, AB’s 9.5% yield is a powerhouse. And with strong fundamentals, it’s more than just a cash cow—it’s a stealth compounder.

Why These 3 Can Beat the Market

Let’s lay it out:

Here’s the secret sauce: dividends reinvested during market downturns are rocket fuel for long-term performance. These stocks don’t just hand you cash—they give you the power to compound.

Plus, when high-yield stocks with solid fundamentals are this discounted (thanks, fear-driven markets!), your downside is cushioned by juicy income. That’s what makes these great rotation plays—as risk-off sentiment increases, and people seek shelter, these types of assets shine.

But Wait—Isn't the S&P 500 Crushing It?

Sure, in 2023 and parts of 2024, the market was on fire, led by mega-cap tech. But here’s the truth bomb: broad-market valuations are stretched, and the S&P’s rally is concentrated in a handful of names.

That spells rotation opportunity.

As rates stay elevated longer than expected, and growth cools off, investors will shift toward:

-

Cash-generating companies

-

High dividends that beat Treasury yields

-

Sectors with real assets and pricing power

This is your window.

How to Play It Smart

A few tips if you’re building a dividend rotation portfolio:

-

Reinvest early: Let compounding do the heavy lifting.

-

Use a tax-advantaged account: MLPs like EPD are better held in taxable accounts, while BDCs and asset managers work well in IRAs or Roths.

-

Don't chase just the highest yield: Focus on payout coverage, growth, and balance sheet strength.

-

Diversify: These three cover energy, finance, and capital markets. That’s a great base.

Conclusion: The Income Engine is Revving

It’s rotation time. And if you’re tired of watching overvalued tech stocks dance on the edge of a macroeconomic cliff, it might be time to lean into real cash flow, fat dividends, and fundamentally sound businesses.

Enterprise Products Partners, Main Street Capital, and AllianceBernstein are three dividend stocks yielding up to 10%—and they’re not just yield traps. They’re part of a smarter play for this market cycle. They offer income, resilience, and the kind of upside that comes from being underestimated.

Because when everyone else is busy chasing hype, the real money is getting paid to wait—and winning anyway.